Global Radio Masts and Towers Market to Reach USD 8.20 Billion by 2033, Expanding at 4.4% CAGR Driven by 5G Infrastructure Rollouts, Network Densification, and Broadcast Modernization: Verified Market Research

Surging demand for telecommunications tower infrastructure, spectrum-driven capacity upgrades, and next-generation broadcast transmission systems underpin steady long-term expansion of the global Radio Masts and Towers Market through the 2025-2033 forecast horizon.

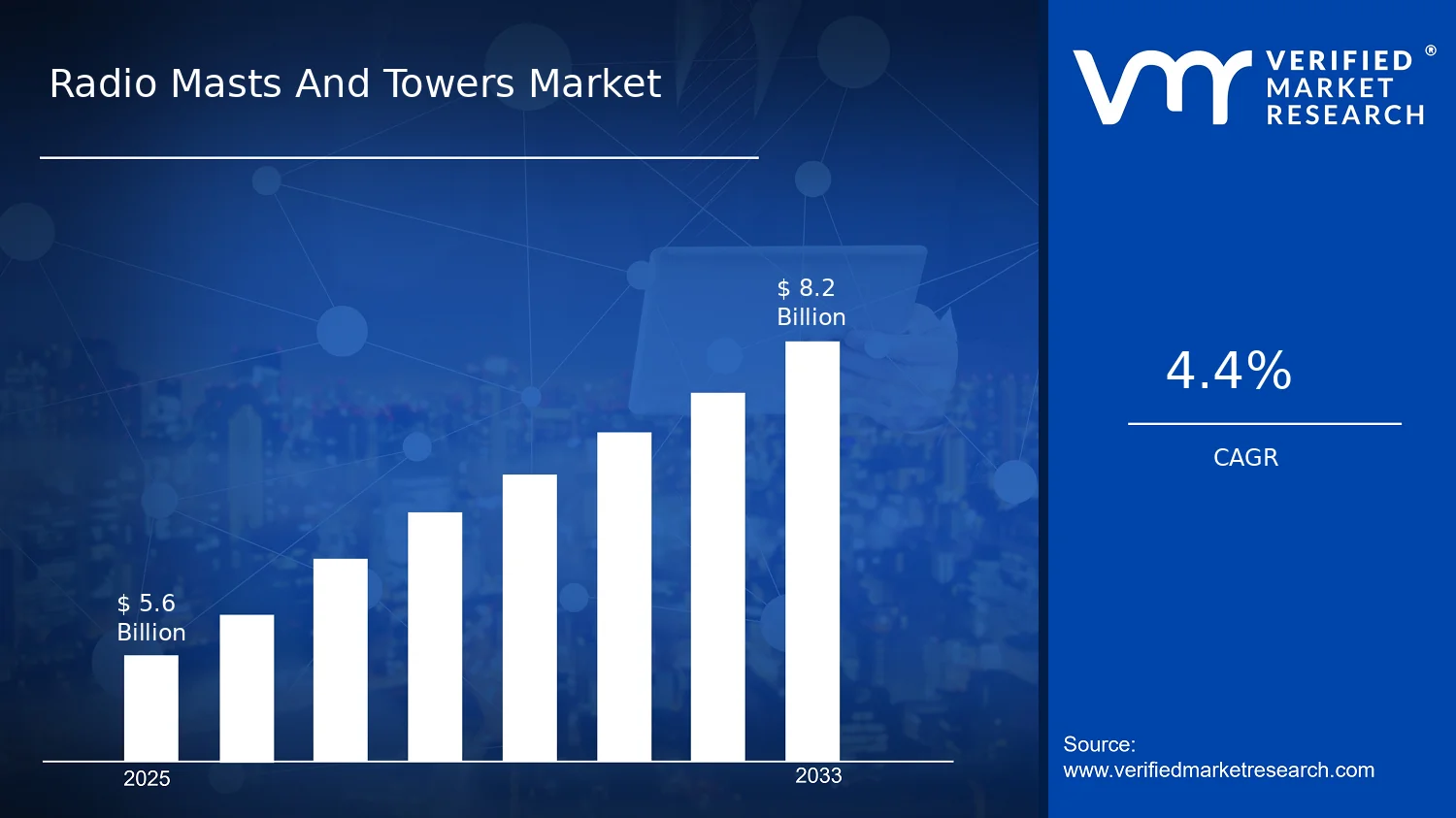

LEWES, DELAWARE, June 08, 2026 (GLOBE NEWSWIRE) -- Verified Market Research®, a leading provider of syndicated market intelligence, announces the release of its comprehensive analysis of the Global Radio Masts and Towers Market. According to the report, the Radio Masts and Towers Market was valued at USD 5.60 Billion in 2025 and is projected to reach USD 8.20 Billion by 2033, expanding at a compound annual growth rate (CAGR) of 4.4% over the forecast period. This steady expansion reflects ongoing network densification programs, infrastructure lifecycle replacement cycles, and the accelerating pace of broadcast and telecommunications modernization across all major global regions.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

The Radio Masts and Towers Market growth trajectory points to a sustained build-out environment rather than a cyclical surge-and-drop pattern. Growth is expected primarily where operators face spectrum-led capacity upgrades and where tower deployment economics favor scalable, compliant structures. Demand is further reinforced by the gradual modernization of broadcast and telecom coverage, including the replacement of aging physical infrastructure and the rollout of new service layers.

Radio Masts and Towers Market Overview

The Radio Masts and Towers Market is defined as the global market for engineered structures designed to support radio frequency transmission and reception for over-the-air communication and broadcast services. The market encompasses the supply and deployment of mast and tower systems whose primary function is to elevate antennas, streamline signal propagation, and provide a structurally reliable platform for broadcast and telecommunications equipment.

Participation in this market includes the design, fabrication, delivery, and installation of radio mast and tower infrastructure, together with the structural components and interface readiness required for mounting antenna, feeder, grounding, and supporting hardware used in live broadcast and network coverage environments. The scope is intentionally anchored on tower and mast infrastructure because the structural engineering choices, procurement processes, and technical qualification requirements distinguish this market from broader broadcast infrastructure categories that blend platform equipment with service operations.

The Radio Masts and Towers Market is segmented by Type (Lattice Towers, Monopole Towers, Guyed Masts, and Stealth Towers), by Installation (Ground-Based and Rooftop), by Application (Telecommunications, Radio Broadcasting, and Television Broadcasting), and by Geography across five key global regions. The report covers 240+ pages of detailed analysis, key player profiles, and forward-looking market forecasts.

Several adjacent markets are explicitly excluded from this analysis, including mobile network radio access network hardware, satellite ground station markets, and general-purpose steel fabrication markets that supply structures without radio-specific antenna support functions. This boundary ensures that Radio Masts and Towers Market sizing aligns precisely with the underlying asset class of engineered mast and tower infrastructure for radio frequency coverage and broadcast transmission.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

Radio Masts and Towers Market Key Growth Drivers

The Radio Masts and Towers Market expansion is driven by an ongoing cause-and-effect chain between coverage needs and physical infrastructure capacity. Several converging forces are accelerating capital investment in new tower builds, upgrades, and refurbishment programs across telecommunications and broadcasting sectors worldwide.

1. Network Densification and Coverage Expansion

Telecom and broadcasting operators continually rebalance network coverage to maintain signal quality at the edge, which translates into demand for additional mounting points, higher elevation, and improved structural performance. As coverage obligations expand and network performance targets tighten, operators replace or augment existing structures to improve signal reach and reduce quality gaps. This drives procurement of engineered tower systems that can support evolving antenna loads and operational requirements. The effect intensifies when upgrade cycles overlap with spectrum-driven planning, causing faster tendering and higher replacement frequency across broadcast and telecommunications footprints.

2. 5G Rollout Intensity and Spectrum-Driven Capacity Needs

Spectrum utilization and channel planning pressures push stakeholders to upgrade radio access and transmission systems, requiring tower and mast assets that can support evolving antenna configurations, feeder arrangements, and link budgets over time. North America leads global 5G deployment activity, driving approximately 35% of Radio Masts and Towers Market share, underpinned by extensive 5G rollouts and high data consumption across the region. The proliferation of 5G requires far denser tower networks than predecessor technologies, creating recurring demand for both new deployments and structural upgrades to existing assets.

3. Regulatory Compliance and Structural Safety Standards

Regulatory expectations around structural integrity, electromagnetic exposure controls, and safety compliance are increasing the share of capital spending devoted to durable, certifiable installations rather than ad hoc fixes. Stricter permitting scrutiny increases the value of documented structural performance, visibility controls, and safety-by-design approaches. This incentivizes bidders to use tower types and installation methods that are easier to certify and configure for site constraints. Over time, operators reduce project uncertainty by standardizing specifications and selecting suppliers with proven compliance pathways, which translates directly into steadier award flow and increased market penetration.

4. Broadcast Infrastructure Modernization

In the broadcast segment, television and radio modernization initiatives create procurement cycles for new transmission sites and selective replacement of obsolete infrastructure. Television and radio broadcasting operators prioritize infrastructure that can accommodate evolving transmission configurations and improve reach, raising the throughput of new installations. These dynamics reinforce demand across both new build and refurbishment programs, with the balance influenced by local permitting timelines and land-use constraints.

5. Material Optimization and Installation Method Evolution

Advances in fabrication practices, corrosion protection, and foundation design are making modern tower options more durable and serviceable. In parallel, improvements in installation planning enable faster ground-based erection and more controlled rooftop integration where space limits growth. The result is lower total cost of ownership and fewer schedule overruns, which supports larger project volumes and more frequent site turnarounds. This ecosystem shift supports faster contracting under regulatory scrutiny and enables operators to align tower design, logistics, and installation planning with network rollouts.

6. Infrastructure Sharing and Long-Term Site Contracts

Cellnex Telecom leads the competitive landscape due to its dense European portfolio and long-term site contracts, a model increasingly adopted across global markets to optimize tower asset utilization. Infrastructure sharing arrangements allow multiple operators to co-locate on the same tower structure, improving return on investment for tower owners and reducing the total number of new structures required while still meeting coverage objectives. This dynamic sustains recurring revenue streams for tower operators and supports steady capital reinvestment in the Radio Masts and Towers Market.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

Emerging Opportunities in the Radio Masts and Towers Market

The Radio Masts and Towers Market presents several high-value opportunity clusters for industry participants, investors, and technology providers over the 2025-2033 forecast horizon.

Rooftop Deployments for Telecom Densification

Rooftop installation opportunities are emerging as operators seek to densify coverage without expanding ground footprints, unlocking faster permitting and shorter lead times for radio mast infrastructure. This shifts project value toward tower designs optimized for structural loads, facade or roof constraints, and rapid integration into existing site infrastructure. Capturing this advantage strengthens competitiveness through execution speed and reduced total installed cost, particularly in dense urban markets where land scarcity constrains ground-based alternatives.

Stealth and Monopole Towers for Urban Coverage

Stealth and monopole towers are increasingly positioned where municipal approvals, community acceptance, or zoning rules constrain conventional structures. The timing is driven by higher scrutiny around cityscape preservation and a growing preference for infrastructure that blends into existing assets. This creates a practical expansion route for vendors that can support compliant configurations, accelerate approvals, and deliver predictable installation outcomes in dense markets where visual impact limits traditional mast and tower options.

Ground-Based Lattice Tower Replacements for Broadcast Resilience

Ground-based upgrades are becoming a clearer opportunity as broadcasting networks prioritize operational continuity, maintenance efficiency, and long-life performance. Lattice towers and guyed masts fit many existing site archetypes, but replacement cycles often stall due to planning uncertainty, limited engineering standardization, or supply constraints at the site level. Vendors that enable faster site readiness, standardized parts, and reliability-focused designs can win repeat programs and expand share across multi-year broadcast network rollout schedules.

Public Safety and Rural Connectivity Funding

Public sector investment in Radio Masts and Towers Market infrastructure is creating significant new demand channels. Planned investment of USD 8 billion for public safety broadband modernization in the United States illustrates how long-horizon commitments can convert into multi-year infrastructure rollouts, including rural and underserved deployment requirements. A complementary program of USD 2 billion over a ten-year horizon targeting territories, tribal nations, and rural regions highlights that expansion extends well beyond dense markets. State-level grants for tower construction, such as USD 7.9 million for improving cellular service in underserved regions, demonstrate how public funding can accelerate site development timelines.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

Radio Masts and Towers Market Challenges and Restraints

Permitting, Licensing, and Site-Approval Delays

Radio Masts and Towers Market deployments depend on approvals tied to spectrum usage, aviation safety checks, environmental review, and local zoning rules. These compliance gates extend scheduling and can require redesigns for setbacks, lighting, and impact mitigation. As lead times stretch, contractors and financiers face higher carrying costs and uncertainty in milestones, which slows procurement cycles and reduces project throughput. The market experiences fewer awarded builds per period, directly limiting adoption scalability across all tower types and installation configurations.

High Total Installed Cost

The installed economics for Radio Masts and Towers Market systems are driven by civil works intensity, transportation constraints, and heavy-lift requirements, especially for ground-based towers. Even when tower materials are available, the full cost structure can strain capital budgets for network operators and broadcasters. This drives more conservative rollout schedules, increases reliance on phased upgrades, and can reduce willingness to expand coverage where demand is uncertain. Profitability pressure also discourages smaller operators from entering new sites.

Operational Complexity During Upgrades

Maintaining service while replacing or upgrading radio mast and tower assets requires careful phasing, temporary transmission arrangements, and structural validation. Performance outcomes depend on height, structural design, wind-loading behavior, and integration with antennas and RF equipment, which adds engineering and commissioning time. If performance risks are perceived as high, buyers extend vendor qualification and testing, delaying final acceptance. This uncertainty reduces adoption speed and can shift demand away from new builds toward incremental fixes.

Supply Chain and Ecosystem Constraints

Supply chains for structural steel, specialized fasteners, and tower components can bottleneck around long lead items, while installation readiness depends on site access, geotechnical data availability, and heavy-lift capacity. Standardization gaps across designs, documentation practices, and grid or RF integration approaches further increase engineering and approval effort. Geographic and regulatory inconsistency across jurisdictions amplifies compliance variability, so timelines and risk premiums differ widely from one region to another.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

Technology and Innovation Trends in the Radio Masts and Towers Market

Higher-Reliability Structural Design

Tower systems are improving through design practices that address real-world variability in wind, corrosion exposure, and long-term fatigue behavior. By refining load modeling, connection design philosophy, and durability-oriented material selection, operators can reduce unplanned downtime and optimize inspection intervals. These changes support more predictable service continuity for telecommunications and broadcasting applications, especially where access for maintenance is limited by security or urban constraints.

Faster, Lower-Disruption Installation Methods

Innovation is emerging in how towers are assembled and erected, shifting the bottleneck from on-site complexity to controlled construction sequences. Improvements in modular fabrication, lift planning, and assembly workflow reduce the number of high-risk activities performed at height or in constrained zones. This increases scalability because project teams can replicate proven installation sequences across multiple sites with fewer schedule deviations, supporting adoption in both commercial rooftops and remote transmission regions.

Evolving Aesthetic and Site-Integration Engineering

Stealth towers and monopole solutions are advancing through design strategies that balance visual integration with structural requirements. Engineering progress focuses on how exterior appearances are achieved while maintaining internal stability paths and access for essential upkeep. When these systems are engineered with site integration in mind, adoption becomes more feasible in densely built geographies and for broadcast operators facing stricter local review processes.

Modularization and Coordinated Delivery Models

Across both ground-based and rooftop deployments, delivery models are increasingly structured to reduce on-site uncertainty by separating complex work into more manageable modules that can be verified before installation. This trend reshapes industry structure by rewarding suppliers and partners that can align schedules across fabrication, shipping, and erection crews, rather than relying on improvisation during site execution. Over time, this reduces variance in project timelines and shifts competitive behavior toward firms with predictable delivery capabilities.

Application-Specific Tower Engineering

Telecommunications, radio broadcasting, and television broadcasting are increasingly treated as different infrastructure categories with distinct operational realities, even when they share similar physical tower environments. This results in more differentiated specification patterns, including how performance expectations are translated into structural choices, configuration constraints, and upgrade pathways. Competitive dynamics evolve as suppliers refine portfolios by application fit rather than competing broadly on generic tower attributes.

Industry Use Cases and End Users

Telecommunications

Telecommunications is the dominant application segment in the Radio Masts and Towers Market due to continued tower demand from mobile networks undergoing capacity and coverage expansion. Telecom operators deploy radio masts and towers primarily to sustain dependable radio coverage and capacity through controlled propagation conditions, accommodating multi-antenna configurations, future carrier additions, and tighter integration with transmission and power equipment. Cell site densification in constrained urban corridors represents a major use case, where operators deploy towers to improve coverage between existing nodes and to support capacity growth without acquiring large new land parcels. U.S. wireless-only capital expenditure is projected to reach USD 33 billion in 2025, indicating a continued willingness to fund new sites and core improvements.

Radio Broadcasting

Radio broadcasting networks use masts and towers to extend program distribution beyond primary transmitters, including relay coverage for rural communities and topographically challenging regions. Systems are placed to maintain reliable signal propagation across planned footprints while withstanding local wind conditions and ensuring stable mounting for radio equipment. Broadcasting rollouts prioritize service continuity and signal distribution consistency, with procurement decisions favoring durable structures that can be maintained on multi-year schedules, including antenna alignment checks and periodic hardware replacement.

Television Broadcasting

Television broadcasting use cases often center on maintaining transmission quality during upgrades to transmission hardware, antenna configurations, or channel planning requirements. Radio masts and towers are selected to support required height profiles and to preserve stability under weather and operational loading, since deviations can affect signal alignment and overall broadcast performance. The compliance and performance verification burden directly affects acceptance cycles, requiring robust testing and validation before full cutover to new infrastructure.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

Regional Outlook: Radio Masts and Towers Market

North America

North America leads the global Radio Masts and Towers Market with approximately 35% market share, driven by extensive 5G rollouts, high data consumption, and mature broadcast network infrastructure. The region's demand profile is characterized by innovation-driven requirements, where operators and broadcasters pursue reliability, coverage continuity, and faster time-to-install rather than basic greenfield expansion. Compliance and permitting are central to project economics, as engineering, public safety, and land-use requirements influence design choices and installation methods. Technology adoption favors engineered lattice and monopole systems that meet structural performance needs while minimizing construction disruption, supporting a sustained baseline of maintenance, replacement, and selective new builds through 2033. North America benefits from comparatively mature fabrication capabilities and established logistics for heavy structures, which reduces uncertainty in lead times for planned upgrades.

Europe

Europe's Radio Masts and Towers Market is shaped by regulation-led engineering discipline, with procurement and design choices heavily influenced by EU-wide harmonization requirements and consistent safety expectations across member states. Cellnex Telecom leads the European competitive landscape due to its dense portfolio and long-term site contracts. The region's mature telecom and broadcasting infrastructure supports demand patterns that prioritize reliability and maintainability over rapid build cycles. Cross-border industrial integration in steel fabrication, specialist tower design, and logistics encourages standardized components and repeatable project delivery practices. Sustainability and environmental compliance pressures influence materials, construction methods, and end-of-life considerations, particularly for long-lived ground-based structures.

Asia Pacific

Asia Pacific plays an expansion-driven role in the Radio Masts and Towers Market, supported by high build-out intensity across telecommunications, radio, and broadcast networks through 2025-2033. The region's demand profile diverges sharply between developed economies such as Japan and Australia, where upgrades and spectral efficiency initiatives dominate, and emerging markets such as India and parts of Southeast Asia, where capacity additions, densification, and greenfield rollout remain the primary growth channels. Rapid industrialization, urbanization, and large population scale increase both site frequency needs and the pace of network modernization. Government-led industrial initiatives raising multi-sector adoption, combined with cost-competitive local manufacturing ecosystems, make Asia Pacific one of the most dynamic regions in the global Radio Masts and Towers Market.

Latin America

Latin America represents an emerging segment of the Radio Masts and Towers Market that expands gradually as telecom modernization and broadcast network upgrades progress. Demand is concentrated in major economies such as Brazil, Mexico, and Argentina, where operators continue to densify coverage and improve transmission reliability. However, purchase cycles are tightly linked to economic conditions, with currency volatility and uneven fiscal environments creating stop-and-go project schedules. Infrastructure constraints, including limited local manufacturing depth and logistics frictions, shape specifications and delivery timelines. Foreign capital and technology partnerships typically enter the region in cycles aligned with broader infrastructure funding and operator consolidation, concentrating demand for higher-specification towers in targeted networks.

Middle East and Africa

Verified Market Research views the Middle East and Africa market as selectively developing rather than uniformly expanding. Gulf economies concentrate demand around telecom and broadcast network modernization tied to national diversification agendas, creating predictable tender cycles for lattice towers, monopole towers, and support structures. Across Africa, infrastructure gaps and uneven industrial readiness create build-where-foundations-exist patterns, increasing reliance on imported tower components and external engineering partners. Radio Masts and Towers demand is more concentrated than widespread, particularly in dense urban centers, national broadcast hubs, and institutional sites. Gradual market formation through public-sector and strategic projects tends to create step changes in demand, but follow-on activity depends on local operational budgets and maintenance ecosystems.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

Competitive Landscape: Radio Masts and Towers Market

The Radio Masts and Towers Market competitive landscape remains moderately fragmented, with scale operators coexisting alongside regional infrastructure specialists. Competition is shaped less by headline pricing and more by project delivery reliability, compliance with RF exposure and structural standards, and the ability to integrate towers and masts into fast-evolving telecommunications networks. Global groups with multi-country asset footprints typically compete on capital access, standardized engineering practices, and long-term tenancy models, while regional entities often win through faster permitting cycles, local right-of-way expertise, and portfolio adjacency to major operators.

Key Company Profiles

American Tower Corporation: Operates primarily as an infrastructure platform provider, translating operator demand into physical tower supply across multiple geographies. Its core activity is the development, acquisition, and management of tower assets that support telecom deployments, with engineering choices that accommodate diverse installation environments and evolving spectrum utilization needs. Differentiation comes from repeatable site development processes and disciplined structural and safety governance.

Crown Castle International Corp.: Positions its competitive strength around wide-ranging network infrastructure management, focusing on sites that support mobile and other radio services in dense and complex environments. Its role is tied to disciplined asset lifecycle management, including structural assurance, configuration flexibility, and the ability to support upgrades over time at existing tower locations.

SBA Communications Corporation: Competes as a specialized tower operator with a portfolio approach aligned to both growth in telecom infrastructure demand and the practical realities of site readiness. Differentiation is expressed through pragmatic selection of locations and repeatable design standards that help projects move through permitting and construction with fewer redesign iterations.

Cellnex Telecom: Operates with a cross-border infrastructure focus emphasizing network-adjacent capabilities and long-term asset utilization. As the market leader in Europe, Cellnex differentiates through portfolio strategy and execution methods designed for consistent operational governance across markets, managing the transition from initial site delivery to ongoing modernization requirements.

Deutsche Funkturm GmbH: Functions as a specialist in broadcast-relevant transmission infrastructure, with competitive positioning influenced by the specificity of broadcasting coverage needs and the operational requirements tied to radio and television transmission continuity. Differentiates through broadcast-grade reliability, site governance, and the capability to support technical evolution without compromising service continuity.

Additional key players in the Radio Masts and Towers Market include American Tower Corporation, Crown Castle International Corp., SBA Communications Corporation, China Tower Corporation, Indus Towers Limited, Bharti Infratel Limited, Helios Towers Africa, IHS Towers, Phoenix Tower International, Vertical Bridge Holdings, LLC, Cellnex Telecom, Inwit S.p.A., Deutsche Funkturm GmbH, Telesites S.A.B. de C.V., Protelindo, Summit Digitel Infrastructure Pvt. Ltd., ATC Europe, Eaton Towers, Tower Bersama Infrastructure Tbk PT, American Tower do Brasil. These players collectively represent a mix of scale operators, regional platform builders, broadcast specialists, and emerging participants with localized deployment strengths.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Radio Masts and Towers Market Sample Report

Radio Masts and Towers Market Segmentation

The Radio Masts and Towers Market is operationally divided across three primary segmentation dimensions: type, application, and installation environment. These segments determine where capital is allocated, how quickly infrastructure is deployed, and which tower configurations win specifications.

By Type

- Lattice Towers - Favored where load-bearing design efficiency and cost discipline are important; frequently aligned with applications requiring strong support for heavier antenna systems and straightforward engineering pathways for multi-device mounting.

- Monopole Towers - Fit urban or constrained sites where footprint and visual integration are deciding factors; lifecycle cost reduction and schedule acceleration are dominant procurement drivers.

- Guyed Masts - Preferred in scenarios where land is available and cost-per-meter can be optimized; the key driver is coverage-driven network expansion where geometry can extend effective reach.

- Stealth Towers - Gain traction in constrained or sensitive visual environments; regulatory and stakeholder acceptance pressures shape procurement, where standard tower visibility faces additional scrutiny.

By Application

- Telecommunications - Dominant segment driven by continued tower demand from mobile networks; capacity upgrade needs drive telecom-led demand as tower systems are selected to support changing antenna loads and performance targets.

- Radio Broadcasting - Reliability and coverage obligations are the primary forces; maintaining consistent signal quality motivates replacement cycles and promotes recurring tower projects aligned to broadcast continuity requirements.

- Television Broadcasting - Network modernization and coverage expansion influence deployments; operators prioritize infrastructure accommodating evolving transmission configurations and improving reach.

By Installation

- Ground-Based - Typically dominates addressable volume due to fewer structural constraints; structural flexibility and foundation planning support ground-based installations as a consistent growth channel.

- Rooftop - Concentrates growth in dense urban zones; space constraint management and faster site access drive rooftop installations as operators limit ground disturbance while meeting performance needs.

By Geography

- North America - ~35% market share; led by the United States with extensive 5G rollouts and high data consumption.

- Europe - Regulation-led market shaped by EU harmonization requirements and cross-border industrial integration.

- Asia Pacific - Expansion-driven region with high build-out intensity across telecommunications, radio, and broadcast networks.

- Latin America - Emerging segment expanding gradually as telecom modernization and broadcast upgrades progress.

- Middle East and Africa - Selectively developing market with concentrated opportunity in Gulf economies and major African urban centers.

Strategic Outlook Through 2033

The Radio Masts and Towers Market is positioned for sustained growth from USD 5.60 Billion in 2025 to USD 8.20 Billion by 2033 at a 4.4% CAGR. This trajectory reflects a market expanding in line with ongoing network buildouts and infrastructure lifecycle replacement, rather than a cyclical surge pattern. For stakeholders assessing the Radio Masts and Towers Market, the key decision signal is that growth is likely sustained through capital expenditure normalization in communications infrastructure, including upgrades requiring new tower assets, refurbishment of existing structures, and increased spectrum usage demands.

The Radio Masts and Towers Market is evolving from a primarily site-driven build model toward a more systems-oriented deployment pattern, with engineering choices increasingly aligned to network planning rather than standalone infrastructure. Over the 2025-2033 period, technology adoption is shifting toward structures that balance installation practicality with predictable performance, influencing how buyers schedule upgrades and how suppliers organize delivery.

Investment activity in the Radio Masts and Towers Market is being directed toward coverage and capacity outcomes, with capital allocation patterns strongly favoring expansion-oriented spending. The emphasis on rural and underserved connectivity increases the durability of demand for ground-based systems, while telecom capex momentum supports multi-year rollout schedules across core tower types. Funding for in-building connectivity is shaping installation preferences and driving differentiation in rooftop and upgrade-focused solutions.

Competitive intensity is expected to evolve toward selective consolidation of portfolios in certain geographies, while specialization by application (telecommunications versus radio broadcasting and television broadcasting) is likely to increase as customers prioritize reliability, compliance, and upgrade continuity alongside physical capacity. Suppliers that align tower type with the operational needs implied by a specific application, and validate that alignment against installation constraints, are best positioned to convert tenders into delivered projects over the forecast horizon.

Overall, the Radio Masts and Towers Market is moving toward greater standardization in how towers and masts are specified and verified, while still allowing specialization by application and geographic context. Stakeholders can prioritize opportunities by aligning scale potential with delivery controllability, weighting short-term wins in repeatable installation categories while reserving investment capacity for segments where technology and qualification barriers create durable differentiation.

Related Reports

Global Military Radio Frequency (RF) Components Market Size By Components (RF Amplifiers, RF Filters), By End-User (Space, Non-Space), By Application (Communication Systems, Radar Systems), By Frequency (Ultra High-Frequency (300MHz-3GHz), Super High-Frequency (3-30 GHz)), By Geographic Scope And Forecast

Global Superconducting Quantum Interferometers Market Size By Type (Direct Current Superconducting Quantum Interference Device (DC SQUID), Radio Frequency Superconducting Quantum Interference Device (RF SQUID)), By Application (Quantum Computing, Medical Imaging), By End-User Industry (Healthcare, Aerospace & Defense), By Geographic Scope And Forecast

Global Professional Mobile Radio Market Size By Technology (Analog PMR Systems, Digital PMR Systems), By Frequency Band (Very High Frequency (VHF), Ultra High Frequency (UHF)), By Application (Public Safety & Law Enforcement, Transportation & Logistics), By Geographic Scope And Forecast

Global Real-Time Location Systems (RTLS) in Transportation and Logistics Market Size By Technology Type (Ultra-Wideband (UWB), RFID (Radio Frequency Identification), Wi-Fi Based Systems, Bluetooth Low Energy (BLE), Infrared, GPS (Global Positioning System)), By Application Area (Fleet Management, Inventory Tracking, Asset Management, Warehouse Management, Cold Chain Monitoring, Supply Chain Visibility), By Component (Hardware, Software, Services) By Geographic Scope And Forecast

Top 6 Radio Frequency Component Companies powering connectivity and innovation

Visualize Radio Masts And Towers Market using Verified Market Intelligence -:

Verified Market Intelligence is our BI Enabled Platform for narrative storytelling in this market. VMI offers in-depth forecasted trends and accurate Insights on over 20,000+ emerging & niche markets, helping you make critical revenue-impacting decisions for a brilliant future.

VMI provides a holistic overview and global competitive landscape with respect to Region, Country, Segment, and Key players of your market. Present your Market Report & findings with an inbuilt presentation feature saving over 70% of your time and resources for Investor, Sales & Marketing, R&D, and Product Development pitches. VMI enables data delivery In Excel and Interactive PDF formats with over 15+ Key Market Indicators for your market.

About Us

Verified Market Research® stands at the forefront as a global leader in Research and Consulting, offering unparalleled analytical research solutions that empower organizations with the insights needed for critical business decisions. Celebrating 10+ years of service, VMR has been instrumental in providing founders and companies with precise, up-to-date research data.

With a team of 500+ Analysts and subject matter experts, VMR leverages internationally recognized research methodologies for data collection and analyses, covering over 15,000 high impact and niche markets. This robust team ensures data integrity and offers insights that are both informative and actionable, tailored to the strategic needs of businesses across various industries.

VMR's domain expertise is recognized across 14 key industries, including Semiconductor & Electronics, Healthcare & Pharmaceuticals, Energy, Technology, Automobiles, Defense, Mining, Manufacturing, Retail, and Agriculture & Food. In-depth market analysis cover over 52 countries, with advanced data collection methods and sophisticated research techniques being utilized. This approach allows for actionable insights to be furnished by seasoned analysts, equipping clients with the essential knowledge necessary for critical revenue decisions across these varied and vital industries.

Verified Market Research® is also a member of ESOMAR, an organization renowned for setting the benchmark in ethical and professional standards in market research. This affiliation highlights VMR's dedication to conducting research with integrity and reliability, ensuring that the insights offered are not only valuable but also ethically sourced and respected worldwide.

Follow Us On: LinkedIn | Twitter | Threads | Instagram | Facebook

Mr. Edwyne Fernandes Verified Market Research® US: +1 (650)-781-4080 US Toll Free: +1 (800)-782-1768 Email: sales@verifiedmarketresearch.com Web: https://www.verifiedmarketresearch.com/ SOURCE - Verified Market Research®

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.